востоковедение

XXI века

мировой экономики

и мировой политики

Source: McKinsey & Company

Source: McKinsey & Company Source: Asia-Pacific Luxury Goods Market (as of 2019)

Source: Asia-Pacific Luxury Goods Market (as of 2019) Luxury Spending in Asia Pacific beyond Coronavirus: Key Strategies for the Future

Luxury Spending in Asia Pacific beyond Coronavirus: Key Strategies for the Future Sources: Gucci “Doraemon” collection; LOEWE x My Neighbor Totoro, a poetic and comforting collaboration

Sources: Gucci “Doraemon” collection; LOEWE x My Neighbor Totoro, a poetic and comforting collaboration Source: McKinsey& Company

Source: McKinsey& Company  Source: WeChat provides a variety of CRMs (2021)

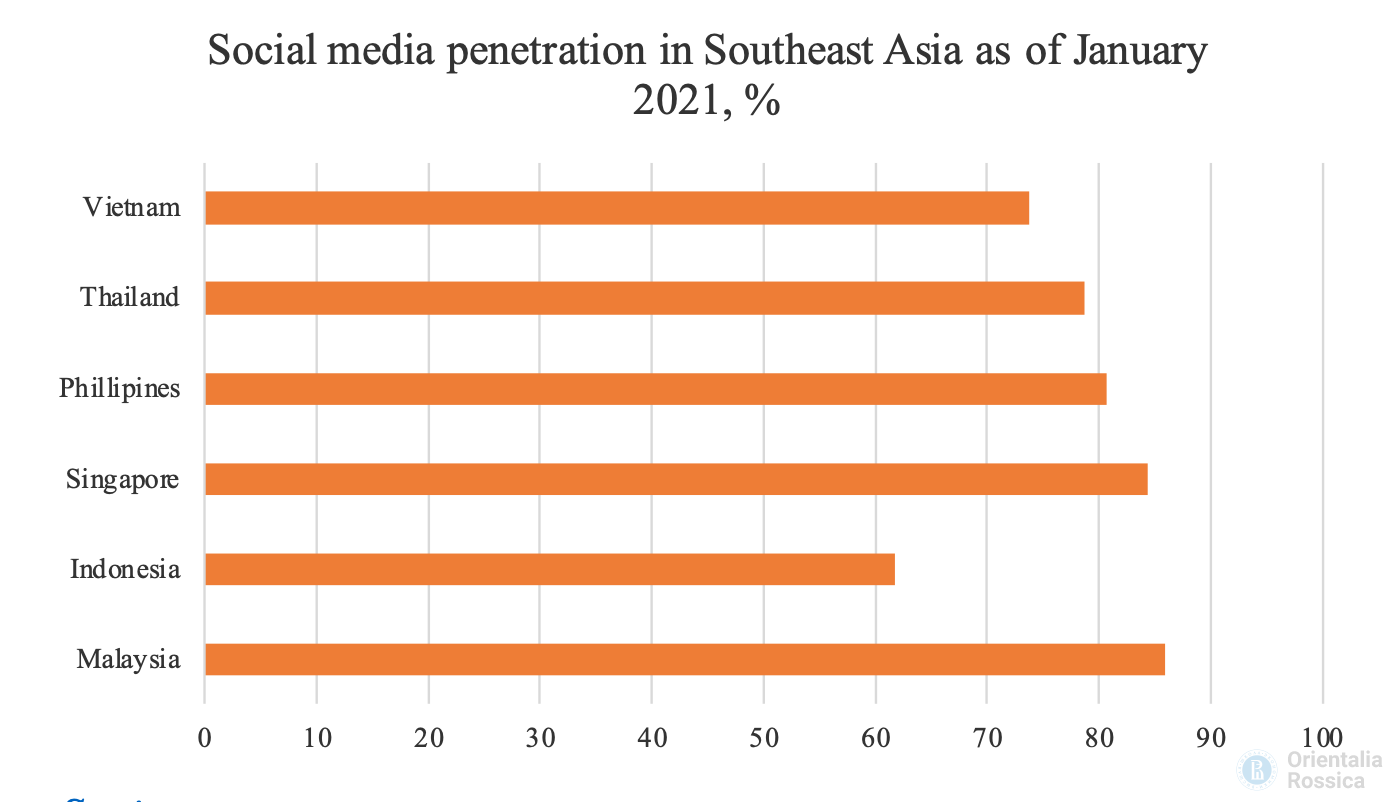

Source: WeChat provides a variety of CRMs (2021) Source: ASEAN Post, Facebook

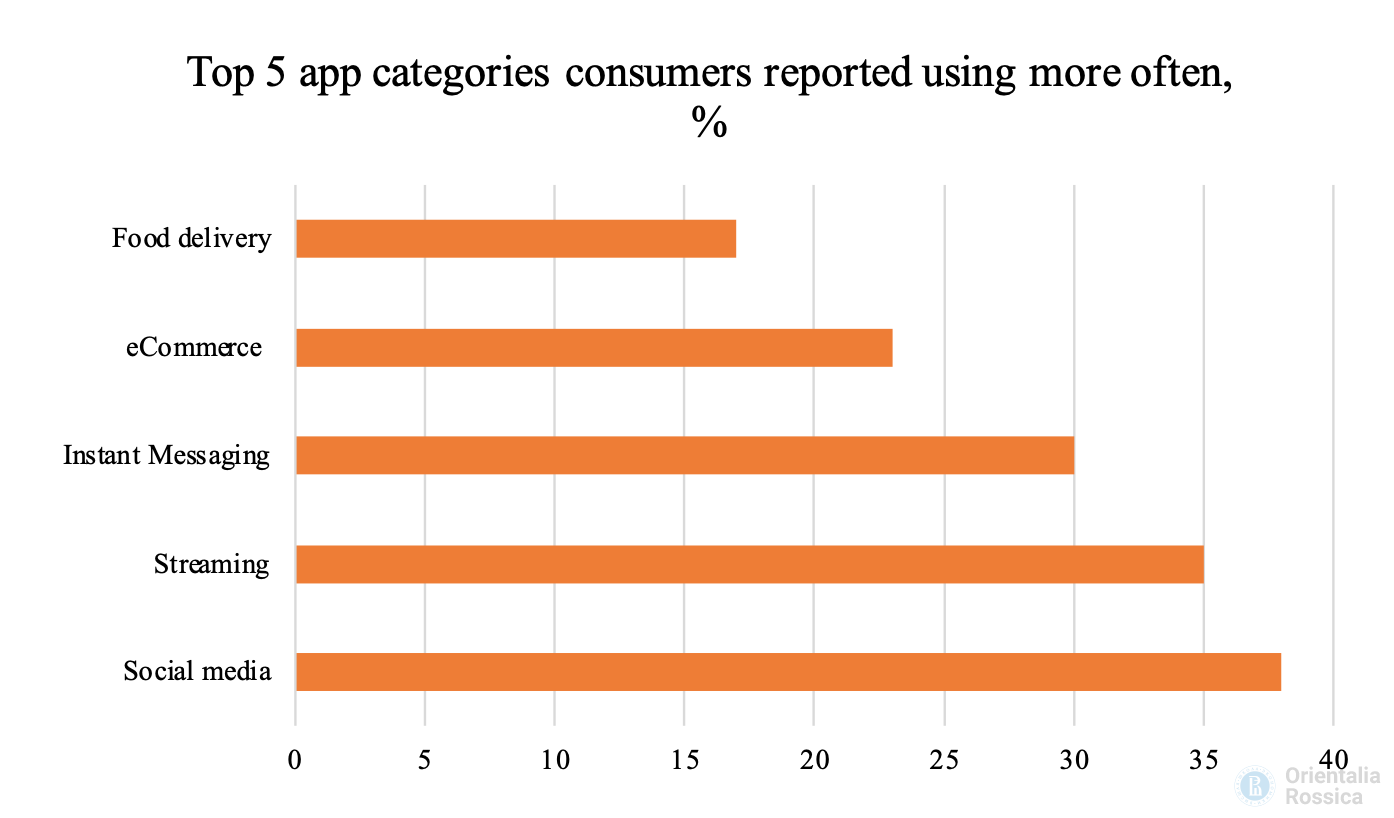

Source: ASEAN Post, Facebook Source: Statista

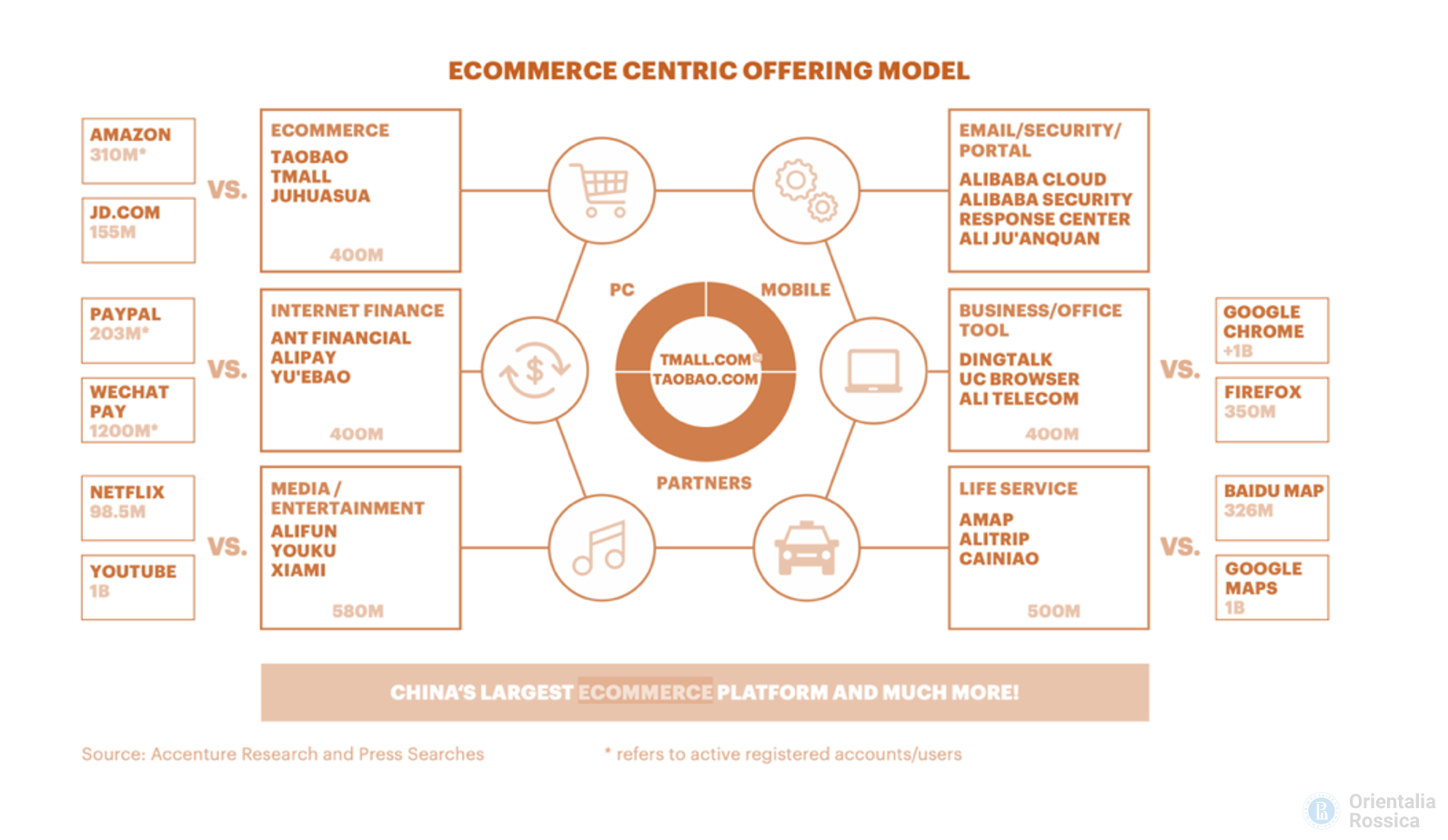

Source: Statista Source: Accenture (2019). Insight Digital Commerce. An APEC Perspective. Accenture, Dublin.

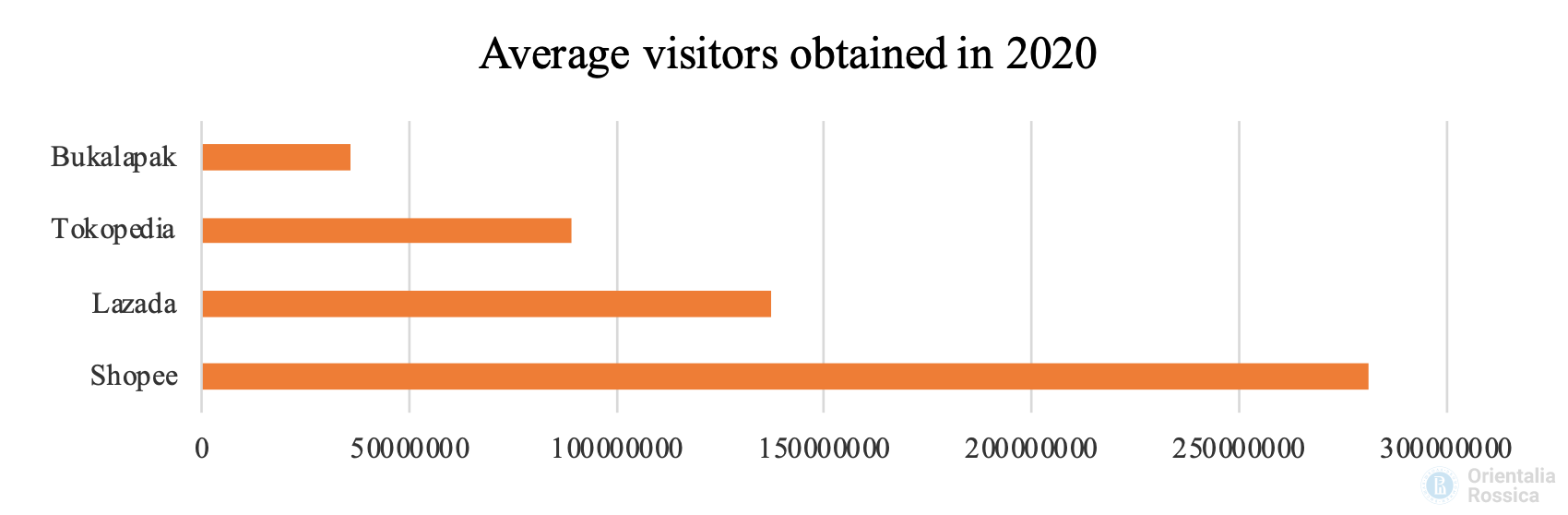

Source: Accenture (2019). Insight Digital Commerce. An APEC Perspective. Accenture, Dublin.  Source: Campaign Asia

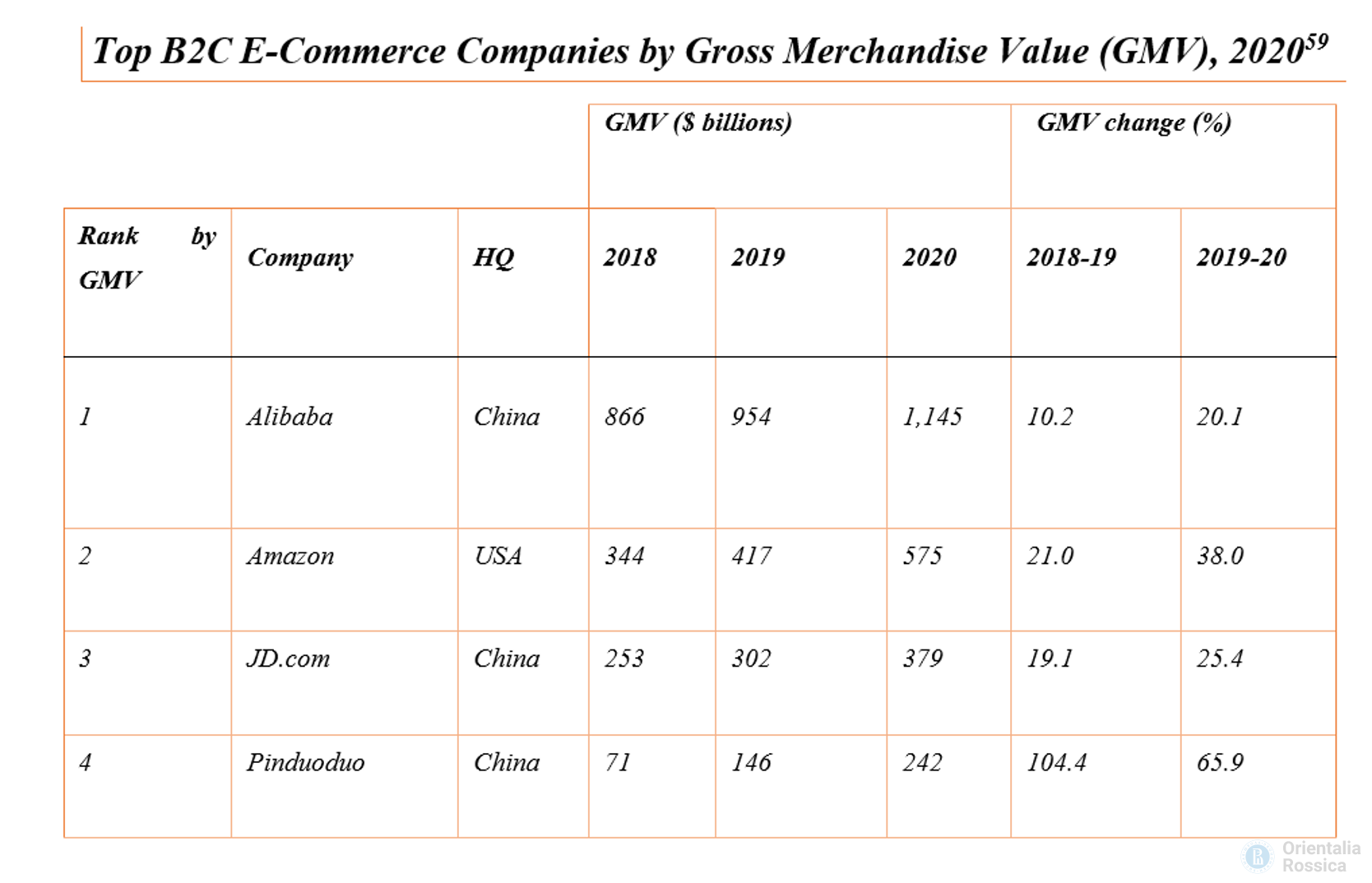

Source: Campaign AsiaAlibaba |

|

|

|

|

AliExpress |

|

|

|

|

Flipkart |

|

HipVan |

|

|

|

JD.com |

|

|

Lazada |

|

|

Qoo10 |

|

|

Rakuten |

|

|

Shopee |

|

|

Snapdeal |

|

Source: Taobao

Source: Taobao Source: Taobao, Alibaba, Flipkart, Technode

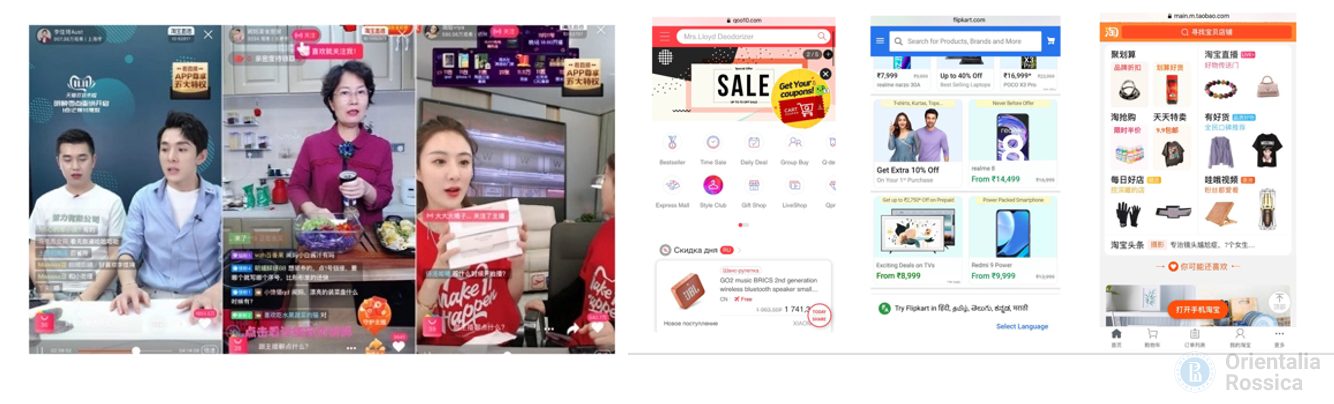

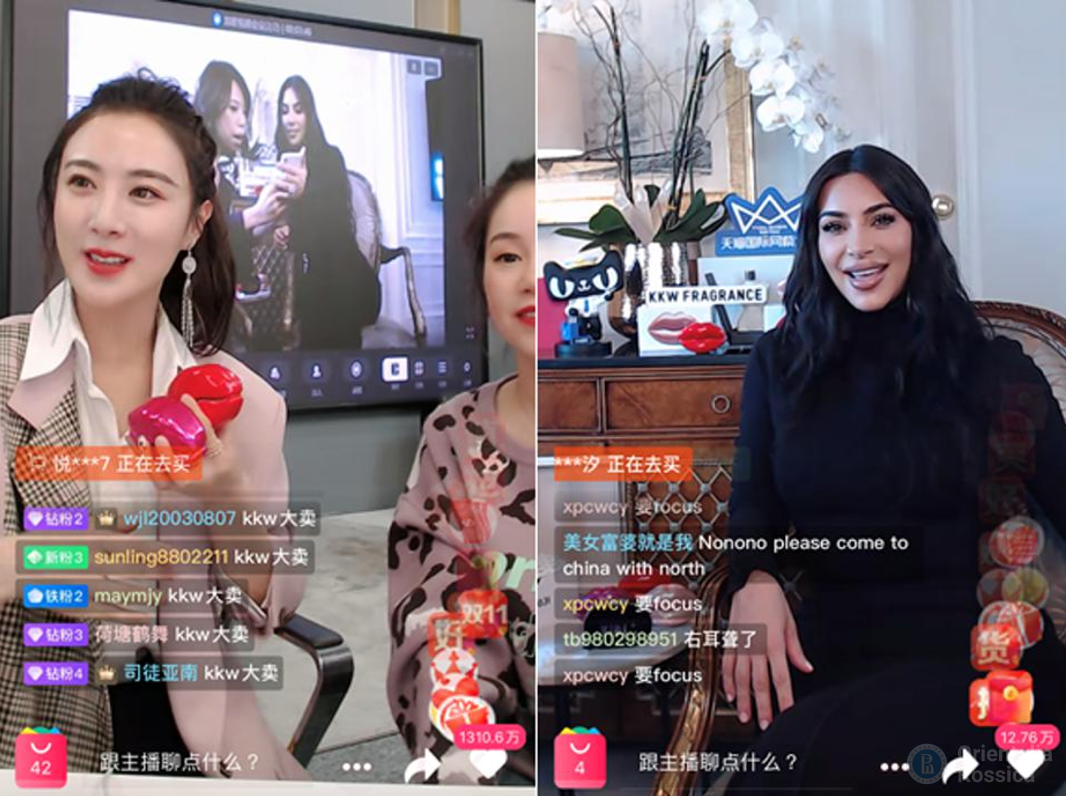

Source: Taobao, Alibaba, Flipkart, Technode  Tmall Live stream in China, 2020

Tmall Live stream in China, 2020 Live stream in China, November 2020

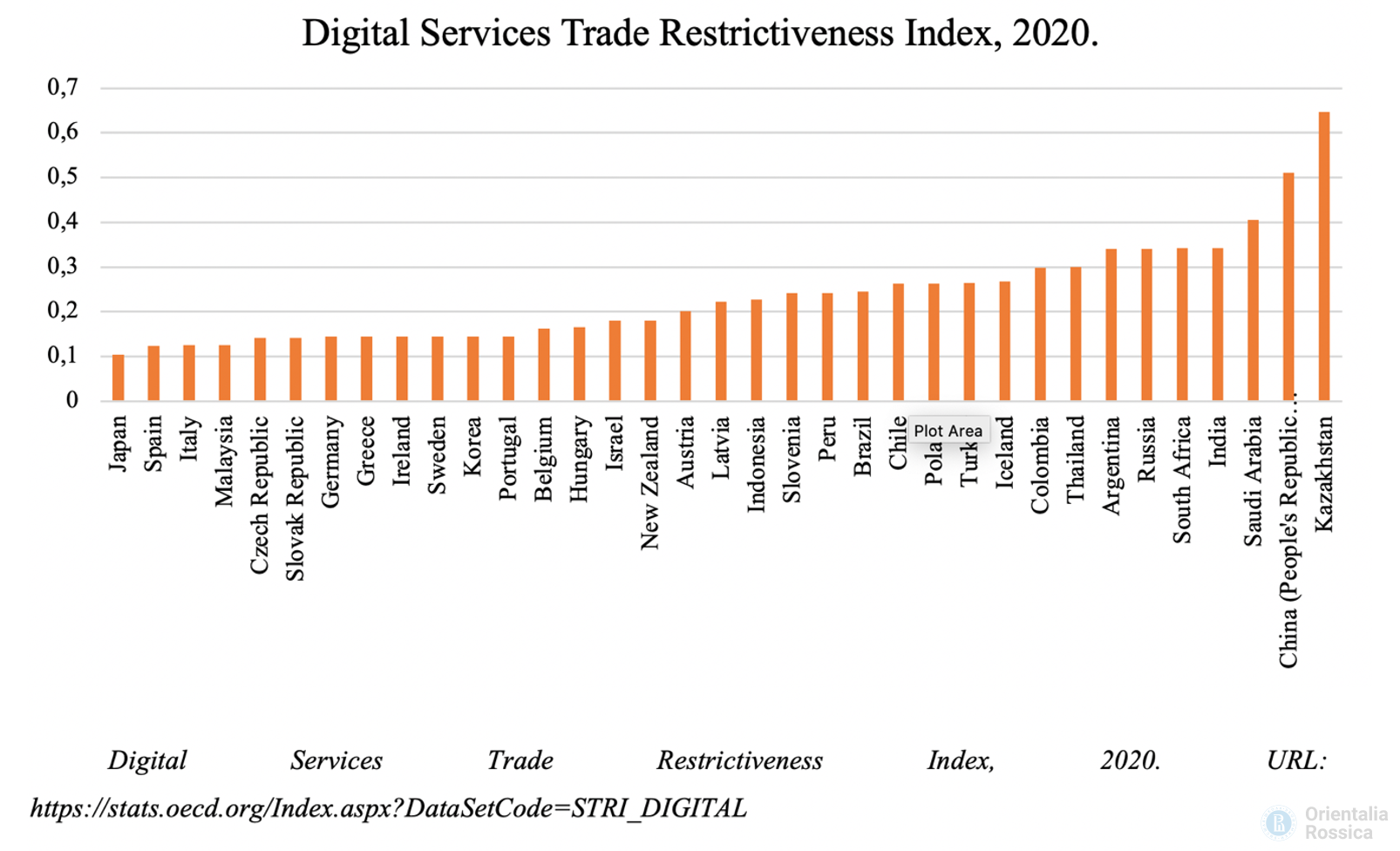

Live stream in China, November 2020 Source: OECD

Source: OECD

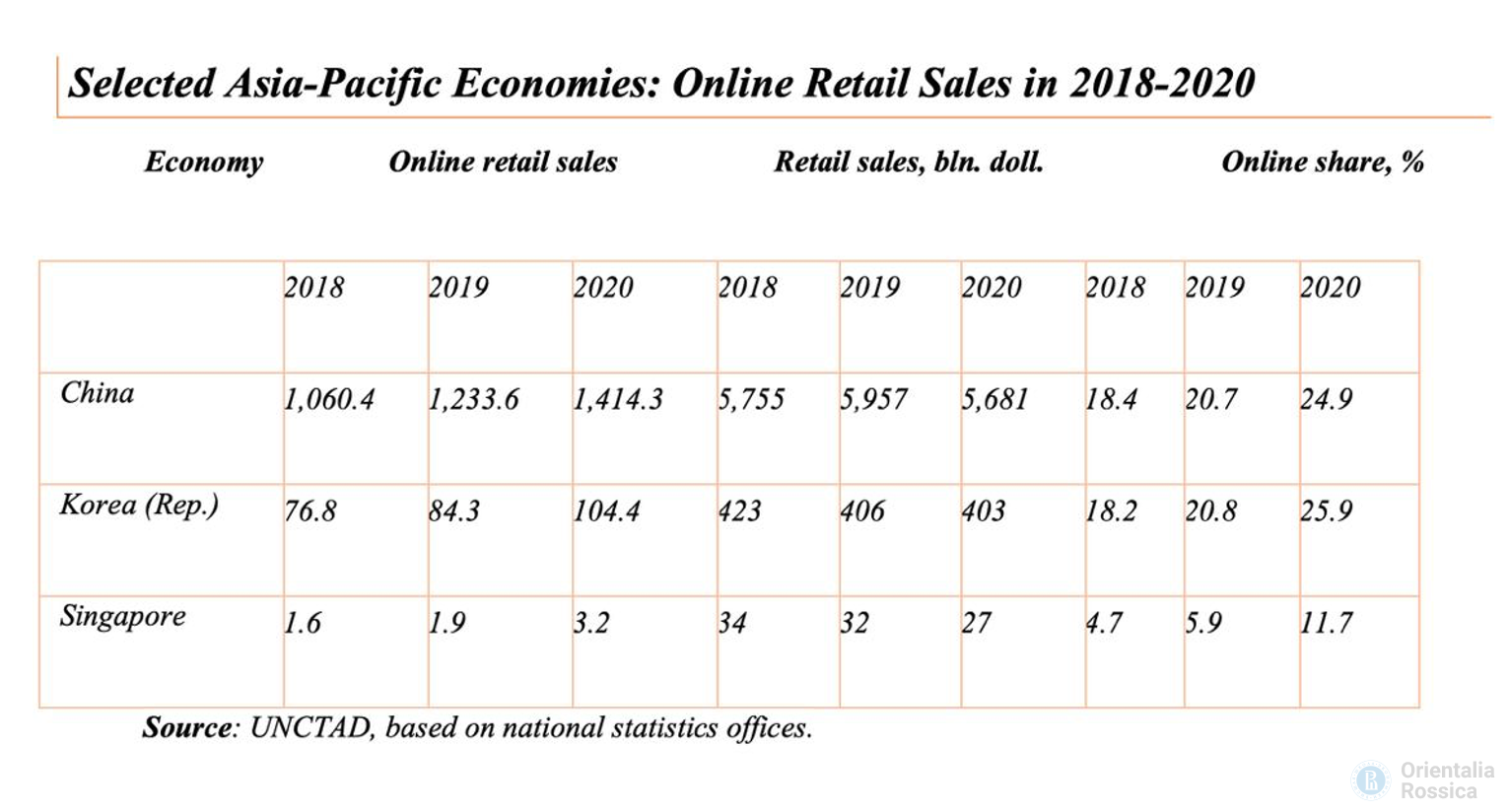

Sources: UNCTAD, UNCTAD Technical notes on ICT Development

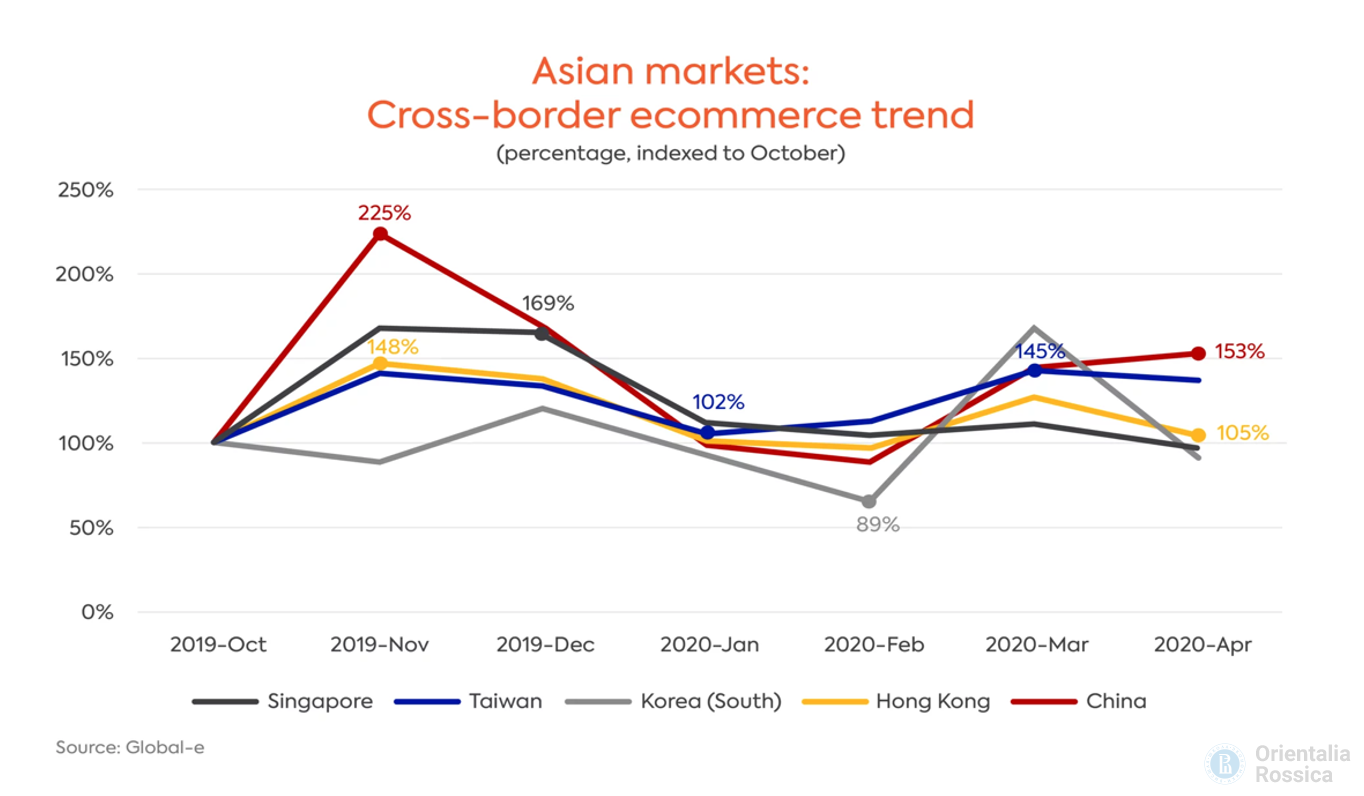

Sources: UNCTAD, UNCTAD Technical notes on ICT Development Source: Global-e, COVID-19: The Impact on Cross-Border Ecommerce

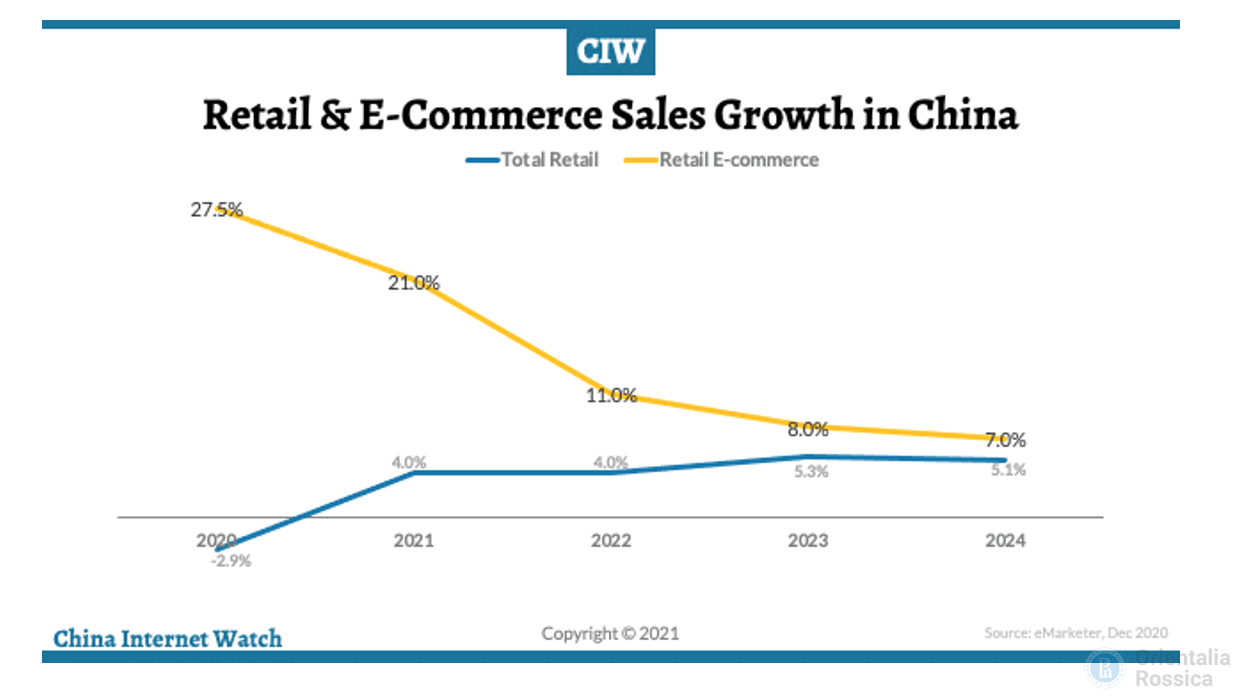

Source: Global-e, COVID-19: The Impact on Cross-Border Ecommerce  Source: China Internet Watch

Source: China Internet Watch

Комментарии

Добавить комментарий